A founder I was auditing pushed back on me recently. I told him that DTC fashion brands typically need to spend 20-25% of revenue on marketing and expansion to grow. His response: “What about Brunello Cucinelli? They closed 2024 with incredible results. And they only spend around 7% on marketing.”

Fair point. So I pulled Cucinelli’s 2024 Annual Report.

The reported communication spend was €92.3 million, or 7.2% of revenue. That looks incredibly efficient. But it’s also incredibly misleading if you stop there.

Because sitting right next to that number in the same investor presentation were two other lines: rent costs (excluded from IFRS 16) of €183.2 million (14.3% of revenue) and personnel costs of €233.5 million (18.3% of revenue).

Cucinelli operates 130 boutiques and 50 hard shops in places like Via Montenapoleone, Sloane Street, Rodeo Drive, and Place Vendôme. That rent isn’t a real estate expense. It’s paying to be physically present where wealthy customers already shop, right next to Hermès and Chanel. It’s customer acquisition through location.

And those boutique staff members in 180 locations across the world’s most expensive cities? They’re doing the same job your Meta ads do: converting browsers into buyers.

Add it up: 7.2% in communication, 14.3% in prime retail rent, plus a significant portion of 18.3% in payroll dedicated to selling. The real customer acquisition cost is well north of 21.5% of revenue. Not 7%.

This pattern repeats across the entire fashion industry. And once you see it, you can’t unsee it.

In this article, I’m going to walk through the financial disclosures of eight major fashion companies: Brunello Cucinelli, Hermès, Prada, Moncler, Burberry, Nike, and Inditex. For each one, I’ll show you what they report as “marketing” and what they actually spend on customer acquisition when you include boutique rent and store staff. The gap between the two numbers is where the real story lives.

Where fashion brands actually spend their marketing budget

Financial statements don’t have a single “customer acquisition cost” line. Instead, what a brand pays to reach and convert customers gets spread across three main buckets.

Advertising and communication covers paid media, brand campaigns, endorsements, and events. This is the number people quote when they say a brand spends “only X% on marketing.”

Boutique rent and occupancy covers prime retail locations and flagship stores. A spot on Via Montenapoleone or Rodeo Drive isn’t real estate. It’s buying impressions from wealthy consumers who walk past your store every day. It’s the physical equivalent of a paid media placement.

Store payroll covers the selling staff and client advisors who convert foot traffic into sales. This cost is almost always buried inside a broader “personnel costs” line that also includes production workers and corporate employees, making it nearly invisible.

Since 2019, IFRS 16 rules require companies to treat leases as if they’re buying the property on credit. Instead of reporting rent as a clear expense, they record an asset and a liability on the balance sheet. The annual cost then shows up as depreciation plus interest, scattered across multiple lines rather than sitting in one “rent” row. This makes it harder to see what a company actually spends on its physical presence. Some brands disclose rent “excluding IFRS 16” (the real cash cost), others only show right-of-use asset depreciation (a proxy). I’ve used the best available figure for each brand and noted the basis.

Most companies don’t split costs cleanly between “boutique” and “everything else.” Personnel often lumps store staff with production and corporate. Rent may include offices alongside retail. I’ve flagged where numbers are precise and where they’re directional. Also, many brands sell through wholesale partners who take 30-50% margins, which is another acquisition cost that never appears as a line item. Where we know the wholesale share, I’ve noted it.

Marketing spend breakdown: 8 fashion brands analyzed

I went through the financial disclosures of eight major fashion companies across luxury, sportswear, and fast fashion. The goal: quantify what each brand actually spends on the full spectrum of customer acquisition (marketing, boutique presence, and selling staff), not just the advertising line.

Brunello Cucinelli (FY2024, revenue €1,278.5M)

Source: FY2024 Results Presentation

| Cost line | Amount | % of revenue |

|---|---|---|

| Investments in Communication | €92.3M | 7.2% |

| Rent costs (excl. IFRS 16) | €183.2M | 14.3% |

| Personnel costs | €233.5M | 18.3% |

| Visible total | €509.0M | ~39.8% |

Cucinelli is the cleanest example in the industry because they disclose all three lines separately in their investor presentations. Almost 40% of revenue goes to communication, stores, and people. Important caveat: personnel costs here include everyone, not just boutique staff. Cucinelli employs artisans, production workers, and corporate teams alongside retail employees. The store-specific portion of payroll would be lower than 18.3%. Similarly, rent may include some non-retail spaces. The precise boutique-only figure is likely smaller, but the overall picture is clear: the real customer-facing cost base dwarfs the 7.2% “marketing” number.

And the table still doesn’t capture everything. 33.4% of Cucinelli’s revenue flows through wholesale partners (department stores, multi-brand retailers) who take their own 30-50% margin. That’s another significant layer of customer acquisition cost that never appears as a line item.

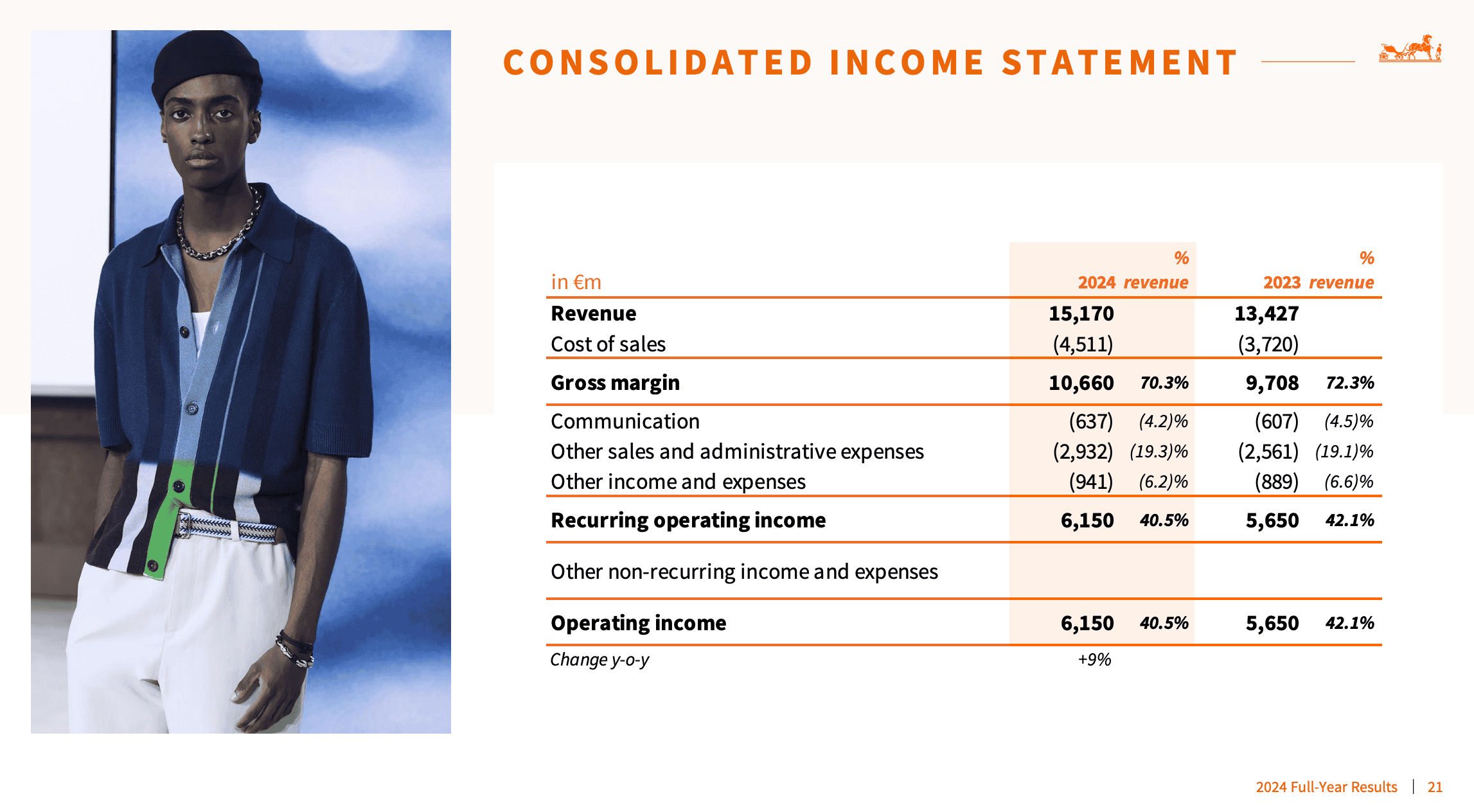

Hermès (FY2024, revenue €15,170M)

Source: Hermès FY2024 Full-Year Results – Hermès FY2024 Presentation

| Cost line | Amount | % of revenue |

|---|---|---|

| Communication | €637M | 4.2% |

| Other sales and admin expenses | €2,932M | 19.3% |

| Visible total (comms + sales/admin) | €3,569M | ~23.5% |

Hermès is arguably the most powerful brand in luxury, and its communication spend is the lowest in the sector at just 4.2% of revenue. If you stopped there, you’d conclude they barely spend anything on growth.

But “other sales and administrative expenses,” which Hermès describes as mainly including “salaries of sales and support staff as well as variable rents,” totals €2.9 billion, or 19.3% of revenue. That line covers the boutique operation, but also includes support functions and administrative staff that aren’t customer-facing. We can’t isolate the boutique-only portion. Still, across 293 stores in 45 countries, the store-related share is substantial.

Hermès also invested €611 million in operating investments for stores and distribution in 2024 alone. That’s capital expenditure on top of the recurring operational costs.

The brand that “barely advertises” actually commits over 23% of revenue to reaching and serving customers. It just doesn’t call it marketing.

Prada Group (FY2024, revenue €5,434M)

Source: Prada Group – Investor Presentation FY 2024 – Prada Group – Press Release FY 2024

| Cost line | Amount | % of revenue |

|---|---|---|

| Advertising and communications | €473.1M | 8.7% |

| ROU asset depreciation (lease proxy) | €454.2M | 8.4% |

| Visible total (ad + lease proxy) | €927.3M | ~17.1%+ |

Prada doesn’t split store payroll from total personnel costs, so this table understates the real total. But with just advertising and a lease proxy, we’re already at 17%+ of revenue. Prada operates 609 stores, and retail (direct stores plus e-commerce) accounts for 89.3% of net revenues.

Worth noting: the lease figure here uses right-of-use asset depreciation as a proxy. The actual cash cost of rent is likely higher. This is one of those cases where accounting standards make fashion brands look leaner than they actually are. And while Prada’s wholesale share is relatively small (8.5% of revenue plus 2.2% in royalties), that’s still a distribution cost embedded in the channel mix rather than visible on the P&L.

Moncler Group (FY2024, revenue €3,108.9M)

Source: FY2024 Annual Report

| Cost line | Amount | % of revenue |

|---|---|---|

| Marketing expenses | €221.2M | 7.1% |

| Rent costs (excl. IFRS 16) | €283.4M | 9.1% |

| Selling personnel costs | €229.4M | 7.4% |

| Visible total | €734.0M | ~23.6% |

Moncler is one of the few companies that separately disclose selling personnel costs (as distinct from total payroll), which gives us an unusually clean picture of the real customer-facing cost base. The rent figure here also specifically sits within selling expenses, making it more boutique-focused than most peers.

Marketing at 7.1% looks lean. Add the rent for boutiques and the people who staff them, and you’re at 23.6% of revenue dedicated to acquiring and converting customers. Because Moncler’s disclosure is more granular than most, this 23.6% is actually one of the more accurate figures in this analysis, with less noise from corporate overhead or production costs.

Burberry (FY2024/25, revenue £2,461M)

Source: FY2024/25 Annual Report

| Cost line | Amount | % of revenue |

|---|---|---|

| Total lease cash outflows | £394M | 16.0% |

| Employee costs | £576M | 23.4% |

| Visible total (lease + employee) | £970M | ~39.4%+ |

Burberry doesn’t break out advertising as a separate P&L line in their financial statements, which makes the “hidden cost” problem even more visible. What we can see: lease payments at 16% of revenue and total employee costs at 23.4%. The employee figure includes corporate, design, and production staff alongside retail teams, so the store-only portion is lower. The lease figure, based on total cash outflows, may also include some non-retail properties. Still, with 422 stores globally, the retail-driven portion is dominant. Together, stores and people consume nearly 40% of revenue before any marketing spend is even counted.

Burberry is also the most instructive case for what happens when revenue drops against this kind of fixed cost base. Revenue fell 15% in FY2024/25. Because boutique leases and staff costs don’t scale down with sales, adjusted operating profit fell 88% to just £26 million (a 1.0% margin). The company is now restructuring under its “Burberry Forward” plan, targeting £100 million in annualised savings, which could affect 1,700 jobs.

When your customer acquisition infrastructure is made of leases and people instead of Meta ads, you can’t just “pause the campaign” when times get tough. The costs keep running.

Nike (FY2025, revenue $46,309M)

Source: FY2025 10-K Annual Report

| Cost line | Amount | % of revenue |

|---|---|---|

| Demand creation expense | $4,689M | 10.1% |

| Visible total | $4,689M | ~10.1%+ |

Nike is useful as a benchmark because they name their marketing spend “demand creation expense” and define it clearly: advertising, digital marketing, brand events, retail brand presentation, endorsements, and athlete contracts. At $4.7 billion, it’s one of the largest marketing budgets in any industry. Nike doesn’t disclose store rent and payroll separately (those sit inside $11.4 billion of “operating overhead”), so we only have the demand creation line here.

What’s telling: in FY2025, Nike’s revenue dropped 10%, but demand creation spending increased 9%. Growth requires investment even when the top line is shrinking.

Inditex (FY2024, revenue €38,632M)

Source: FY2024 Annual Results

| Cost line | Amount | % of revenue |

|---|---|---|

| Personnel expenses | €4,557M | 11.8% |

| Rental expenses | €1,781M | 4.6% |

| Visible total (personnel + rental) | €6,338M | ~16.4%+ |

Inditex is the efficiency benchmark. Personnel at 11.8% and rental at 4.6% are notably lower than luxury peers. Both figures include some non-store costs (headquarters, logistics), but with 5,563 stores across 39 markets, retail is the dominant component.

Even the most efficient fashion retailer on the planet spends over €6.3 billion annually on people and locations. Inditex doesn’t separately disclose advertising (it’s known to be minimal). Their acquisition model is built on location strategy, product rotation speed, and in-store experience rather than paid media. Different mechanism, same principle.

Fashion brand marketing spend compared

| Brand | Segment | Marketing | Boutique rent | Store payroll | Min. visible total |

|---|---|---|---|---|---|

| Brunello Cucinelli | Luxury | 7.2% | 14.3% | 18.3%* | ~39.8% |

| Hermès | Luxury | 4.2% | — | — | ~23.5%** |

| Prada Group | Luxury | 8.7% | 8.4%† | n/d | ~17.1%+ |

| Moncler | Luxury outerwear | 7.1% | 9.1% | 7.4% | ~23.6% |

| Burberry | Premium luxury | n/d | 16.0%‡ | 23.4%* | ~39.4%+ |

| Nike | Sportswear | 10.1% | — | — | ~10.1%+ |

| Inditex | Fast fashion | n/d | 4.6% | 11.8%* | ~16.4%+ |

| *Total personnel (includes production, corporate, and admin staff alongside retail). **Hermès “other sales and admin” combines rent + store staff + support functions. †ROU depreciation proxy, likely understates actual rent. ‡Lease cash outflows, may include some non-retail properties. | |||||

*Total personnel (includes production, corporate, and admin staff alongside retail). *Hermès “other sales and admin” combines rent + store staff + support functions. †ROU depreciation proxy, likely understates actual rent. ‡Lease cash outflows, may include some non-retail properties.

These are disclosed minimums, and most figures include non-retail costs that inflate the percentages. But even accounting for that, every brand dedicates a substantial share of revenue to the machinery of reaching, converting, and serving customers. And where brands sell through wholesale (Cucinelli at 33.4%, Burberry at ~13%), there’s an additional layer of acquisition cost embedded in the partner’s margin that doesn’t appear here at all.

The brands that report “low marketing spend” are simply paying the same bill under different names.

What this means if you’re building a fashion brand

The brands in this article aren’t overspending. They’re spending what it costs.

When someone tells me Brunello Cucinelli “only spends 7% on marketing,” they’re reading one line of a financial statement and ignoring the other 30%+ doing the same job under different names. When someone points to Hermès and its 4.2% communication budget, they’re ignoring the €2.9 billion line that funds 293 stores and thousands of client advisors.

The mechanism changes depending on the model. DTC brands pay Meta and Google. Luxury houses pay landlords and staff. Wholesale brands give up 30-50% margin to retail partners. Same function. Different line items.

This is why I keep pushing on margins, positioning, and unit economics before anything else. If your gross margins can’t sustain a 20-25% customer acquisition cost (however it’s structured), you don’t have a growth problem. You have a business model problem.

There is no shortcut. You either pay for growth, or you don’t grow.